This article is a summary version of FIRSTLIGHT “SaaS Annual Report 2024-2025,” which provides an overview of the Japanese SaaS market and trends.

The full report (24 pages) can be downloaded from the form at the bottom of this article

On publication of the SaaS Annual Report

Osamu Iwasawa, CEO/Managing Partner, FIRSTLIGHT Capital, Inc.

In 2024, amid advancing AI technology and rising expectations, the phrase “SaaS is dead” gained attention. Is SaaS really coming to an end?

When the emergence of AI agents makes it possible to mass-produce software, oversupply and price competition will be inevitable. SaaS solutions that are not a must-have for users will be quickly eliminated. The Japanese SaaS industry, which has been somewhat idyllic until now, will be forced to confront the fundamental value of its products, entering a period of survival of the fittest.

This change signifies a major shift in the very rationale of SaaS, and entrepreneurs, investors, and all other stakeholders will be pressed to rethink their existing approaches.

How will conventional SaaS merge with AI? 2025 will be a turning point that sets the future direction.

This year, the Tokyo Stock Exchange presented upcoming revisions in continued listing criteria for the Growth Market. Companies that fail to reach a market capitalization of JPY 10 billion within five years from IPO will be delisted under the new policy.

To meet this threshold, companies will need to grow their businesses even faster than before, making IPOs even more challenging. Going forward, we expect to see more early-stage startups discussing M&A options, both as buyers and sellers.

This report provides an overview of the current state and changes in the SaaS market and includes the latest data to support decision-making. The “Overview” section outlines the current state of the SaaS market, followed by “Feature 1: Funding for SaaS Startups,” and “Feature 2: The Current State and Winning Strategies of Domestic AI Startups.”

Amid accelerating shifts in technology and capital markets, Japan faces a number of challenges, including a shrinking workforce and industrial restructuring.

The question now is whether startups can provide new value to address these challenges.

– Overview –

While 2024 has followed the trends of previous years, new developments have also been observed.

We have compiled an overview of quantitative analysis from various perspectives, including ARR, multiples, IPOs, private fundraising, M&A, and ARR acquisition efficiency.

Here, we excerpt selected parts of the report and provide commentary.

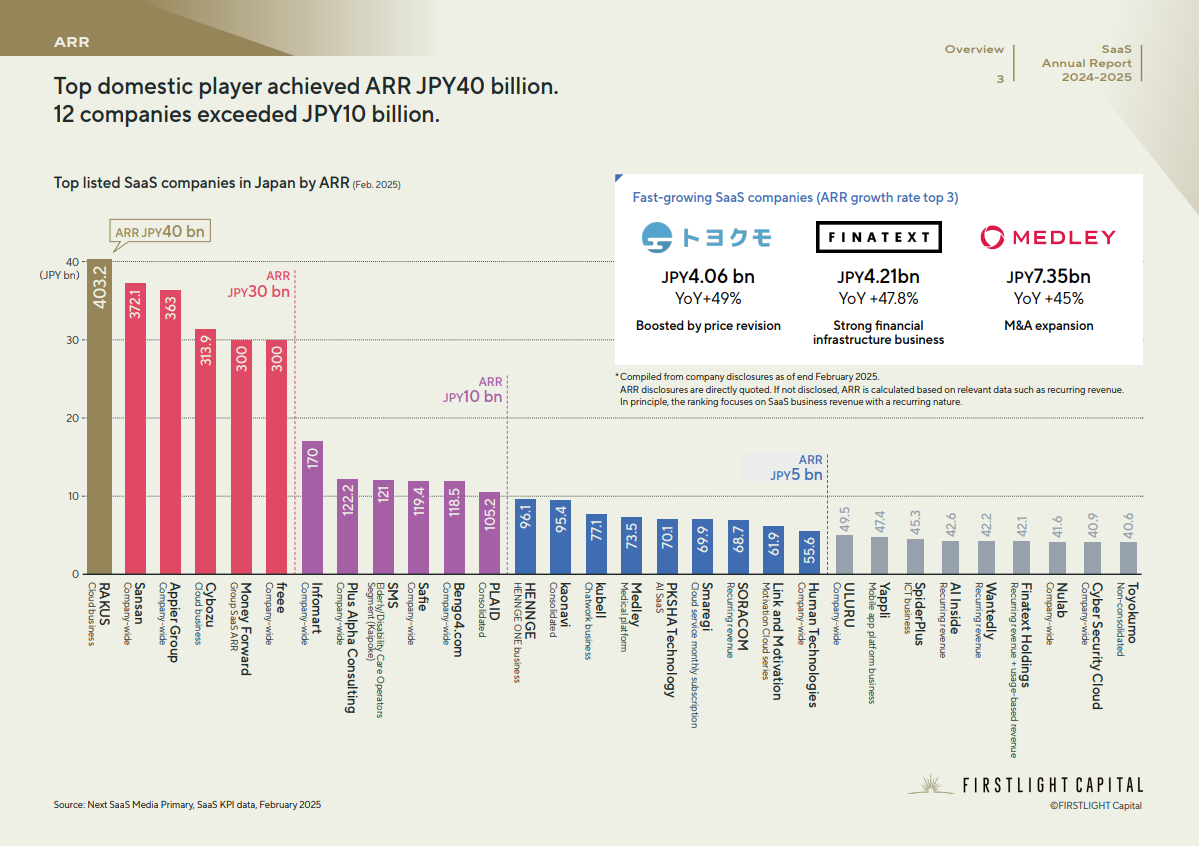

1. ARR:Top domestic player achieved ARR JPY40 billion. 12 companies exceeded JPY10 billion.

Top SaaS companies are showing continuous growth, with some reaching an ARR JPY 40 billion.

On the other hand, the gap in ARR between the top companies and those in the middle and lower ranks is widening.

The top five companies, such as RAKUS and Sansan, have demonstrated remarkable “sustainable growth,” with a five-year CAGR of over 25% after exceeding an ARR JPY 10 billion.

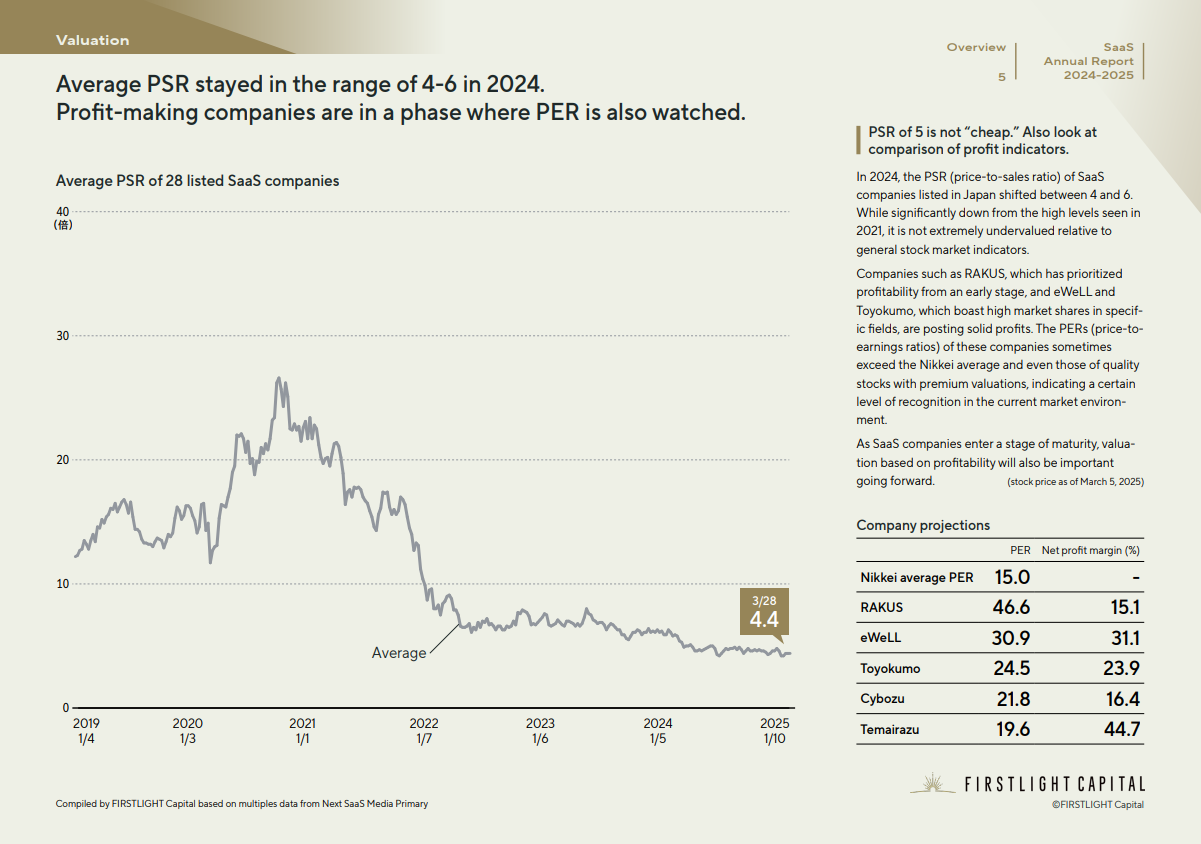

2. Valuation:Average PSR stayed in the range of 4-6 in 2024. Profit-making companies are in a phase where PER is also watched.

In 2024, the PSR (price-to-sales ratio) of SaaS companies listed in Japan shifted between 4 and 6.

While significantly down from the high levels seen in 2021, it is not extremely undervalued relative to general stock market indicators.

Companies such as RAKUS, which has prioritized profitability from an early stage, and eWeLL and Toyokumo, which boast high market shares in specific fields, are posting solid profits.

The PERs (price toearnings ratios) of these companies sometimes exceed the Nikkei average and even those of quality stocks with premium valuations, indicating a certain level of recognition in the current market environment.

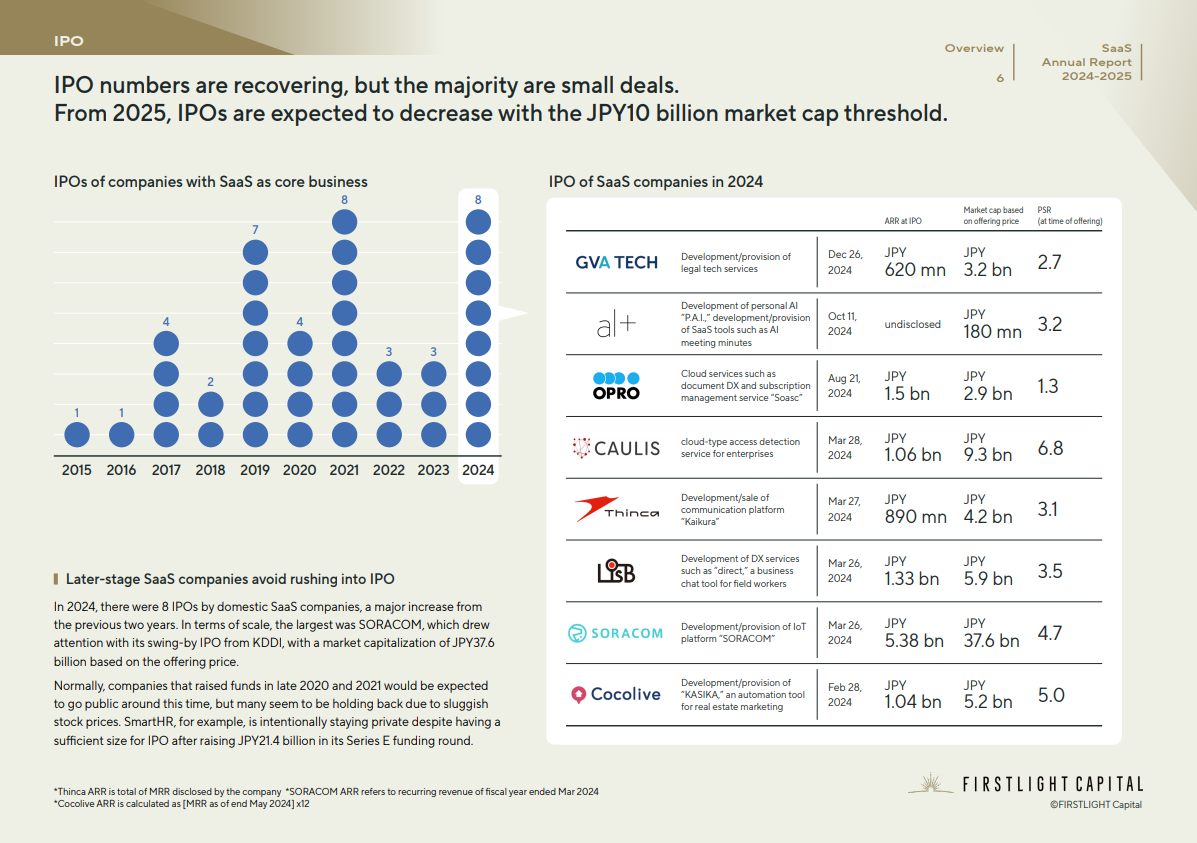

3. IPO:IPO numbers are recovering, but the majority are small deals.

From 2025, IPOs are expected to decrease with the JPY10 billion market cap threshold.

In 2024, there were 8 IPOs by domestic SaaS companies, a major increase from the previous two years.

In terms of scale, the largest was SORACOM, which drew attention with its swing-by IPO from KDDI, with a market capitalization of JPY37.6 billion based on the offering price.

Normally, companies that raised funds in late 2020 and 2021 would be expected to go public around this time, but many seem to be holding back due to sluggish stock prices.

SmartHR, for example, is intentionally staying private despite having a sufficient size for IPO after raising JPY21.4 billion in its Series E funding round.

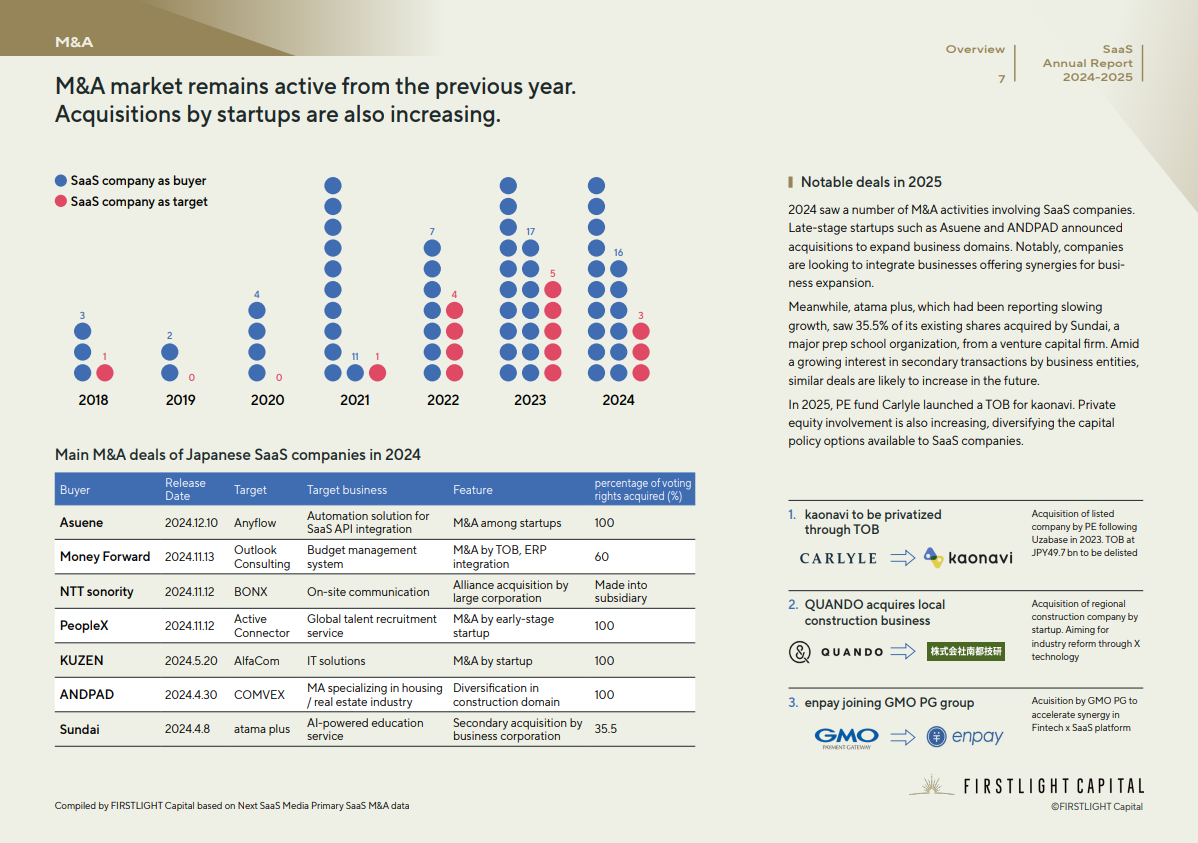

4. M&A:M&A market remains active from the previous year.

Acquisitions by startups are also increasing.

2024 saw a number of M&A activities involving SaaS companies.

Late-stage startups such as Asuene and ANDPAD announced acquisitions to expand business domains. Notably, companies are looking to integrate businesses offering synergies for business expansion.

In 2025, PE fund Carlyle launched a TOB for kaonavi. Private equity involvement is also increasing, diversifying the capital policy options available to SaaS companies.

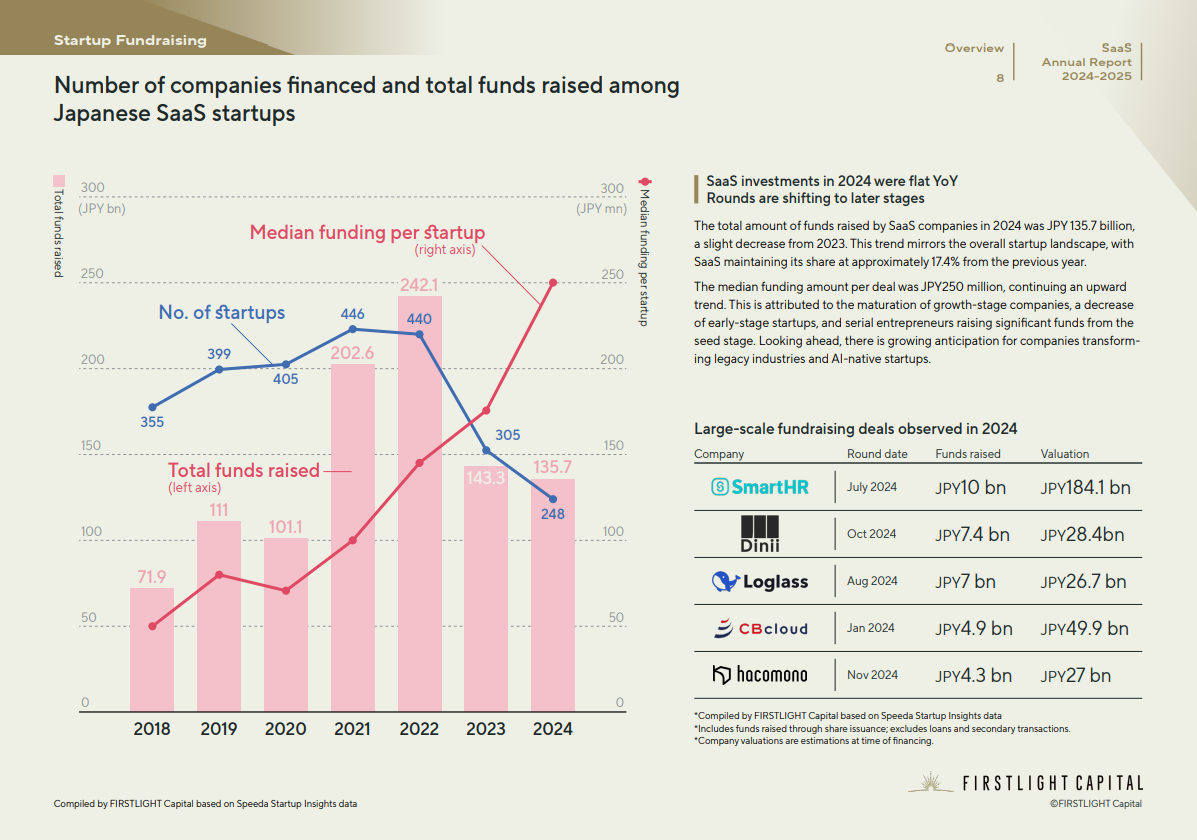

5. Startup Fundraising:Number of companies financed and total funds raised among Japanese SaaS startups.

The total amount of funds raised by SaaS companies in 2024 was JPY 135.7 billion, a slight decrease from 2023. This trend mirrors the overall startup landscape, with SaaS maintaining its share at approximately 17.4% from the previous year.

The median funding amount per deal was JPY250 million, continuing an upward trend. This is attributed to the maturation of growth-stage companies, a decrease of early-stage startups, and serial entrepreneurs raising significant funds from the seed stage.

– Vertical SaaS –

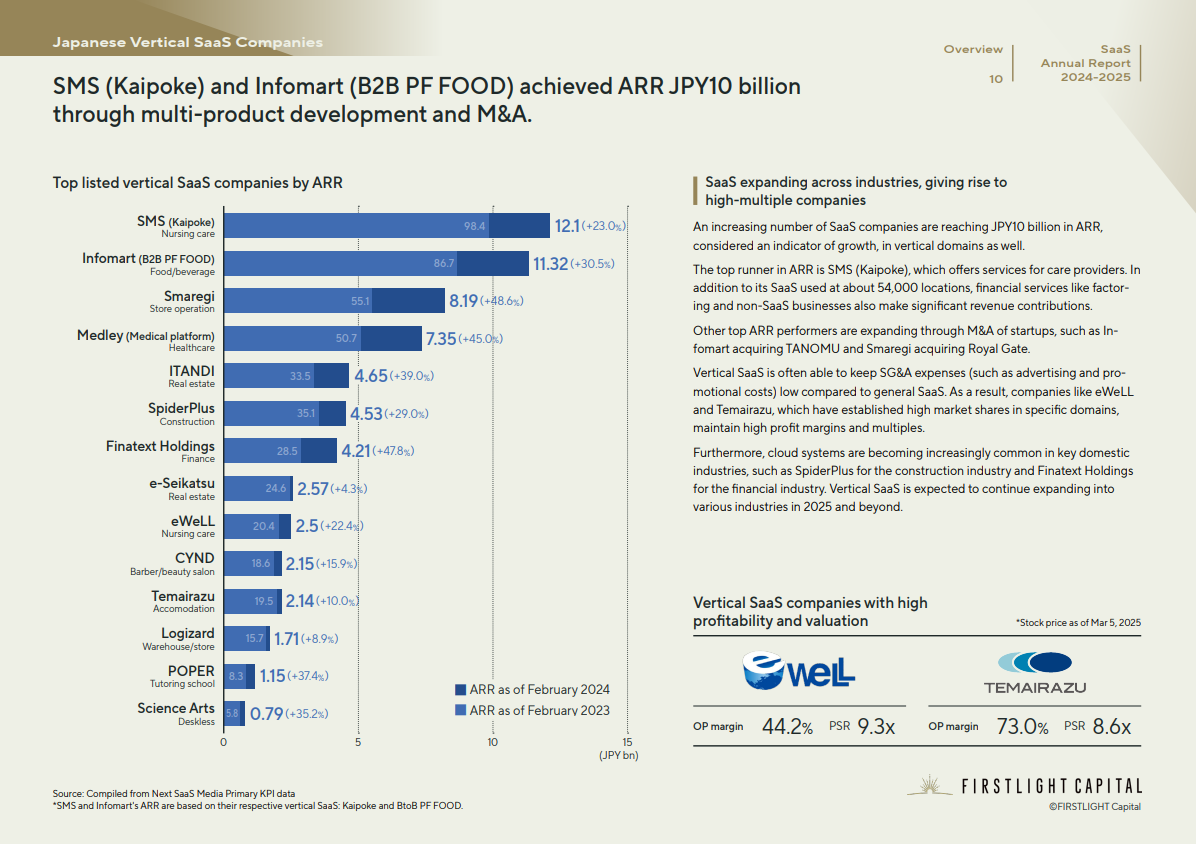

6. SMS (Kaipoke) and Infomart (B2B PF FOOD) achieved ARR JPY10 billion through multi-product development and M&A.

An increasing number of SaaS companies are reaching JPY10 billion in ARR, considered an indicator of growth, in vertical domains as well.

The top runner in ARR is SMS (Kaipoke), which offers services for care providers.

In addition to its SaaS used at about 54,000 locations, financial services like factoring and non-SaaS businesses also make significant revenue contributions.

Vertical SaaS is often able to keep SG&A expenses (such as advertising and promotional costs) low compared to general SaaS.

As a result, companies like eWeLL and Temairazu, which have established high market shares in specific domains, maintain high profit margins and multiples.

Vertical SaaS is expected to continue expanding into various industries in 2025 and beyond.

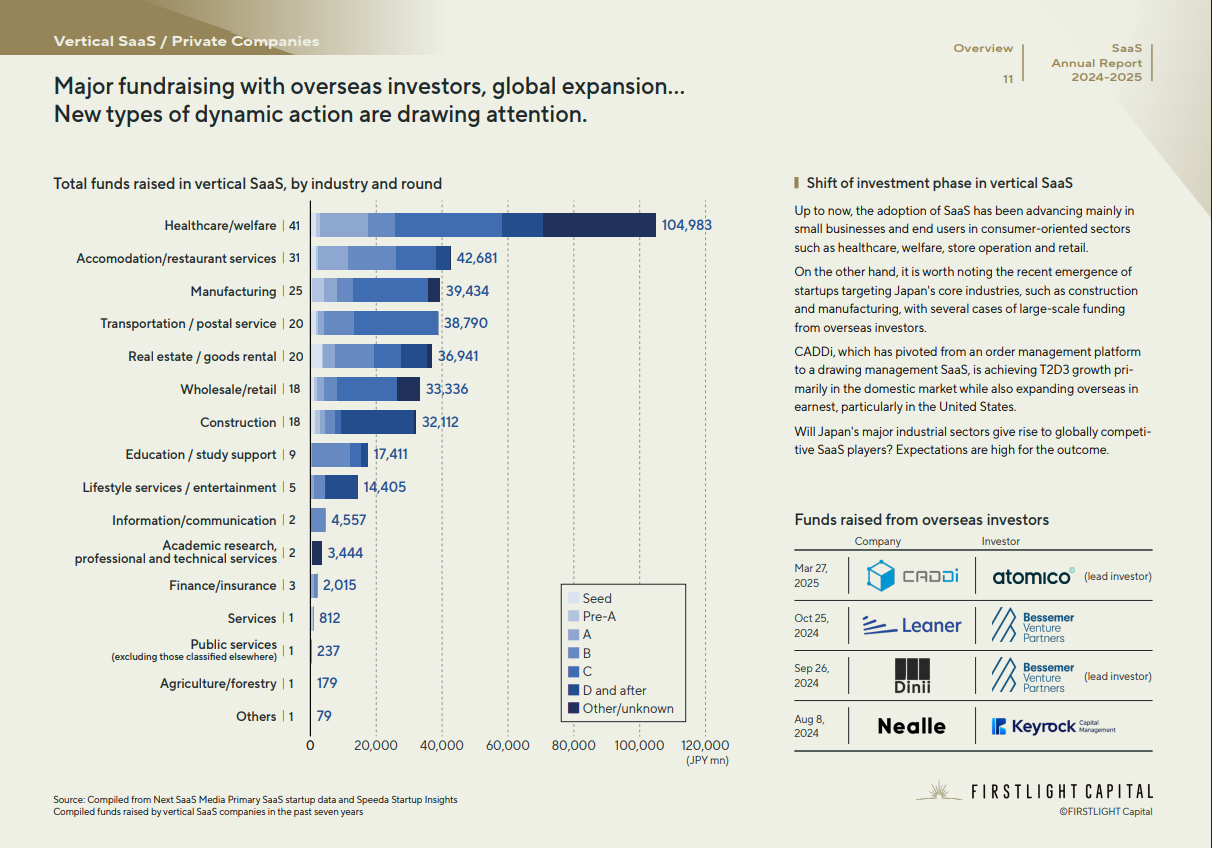

7. Vertical SaaS Fundraising:Major fundraising with overseas investors, global expansion… New types of dynamic action are drawing attention.

Up to now, the adoption of SaaS has been advancing mainly in small businesses and end users in consumer-oriented sectors such as healthcare, welfare, store operation and retail.

On the other hand, it is worth noting the recent emergence of startups targeting Japan’s core industries, such as construction and manufacturing, with several cases of large-scale funding from overseas investors.

CADDi, which has pivoted from an order management platform to a drawing management SaaS, is achieving T2D3 growth primarily in the domestic market while also expanding overseas in earnest, particularly in the United States.

– Feature 1 – SaaS Startup Fundraising Analysis

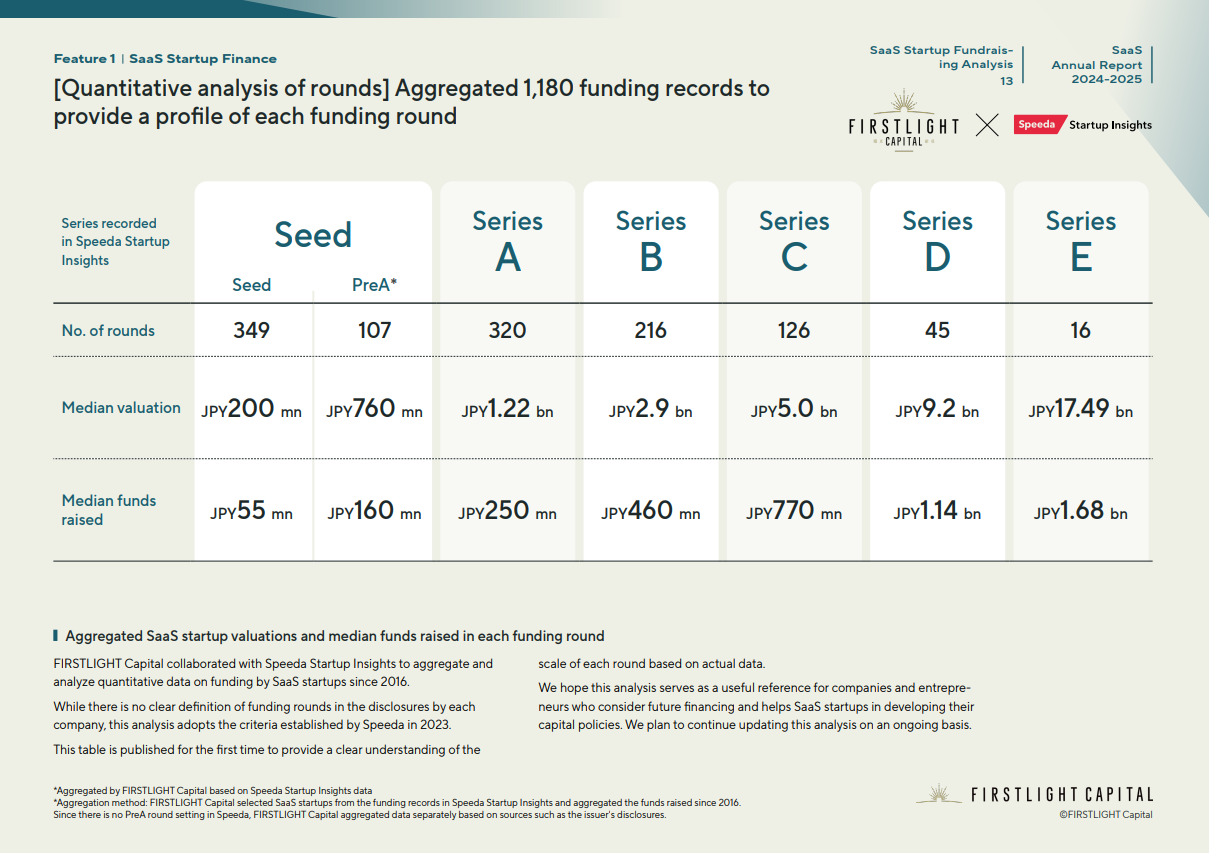

8. [Quantitative analysis of rounds] Aggregated 1,180 funding records to provide a profile of each funding round

FIRSTLIGHT Capital collaborated with Speeda Startup Insights to aggregate and analyze quantitative data on funding by SaaS startups since 2016.

While there is no clear definition of funding rounds in the disclosures by each company, this analysis adopts the criteria established by Speeda in 2023.

This table is published for the first time to provide a clear understanding of the scale of each round based on actual data.

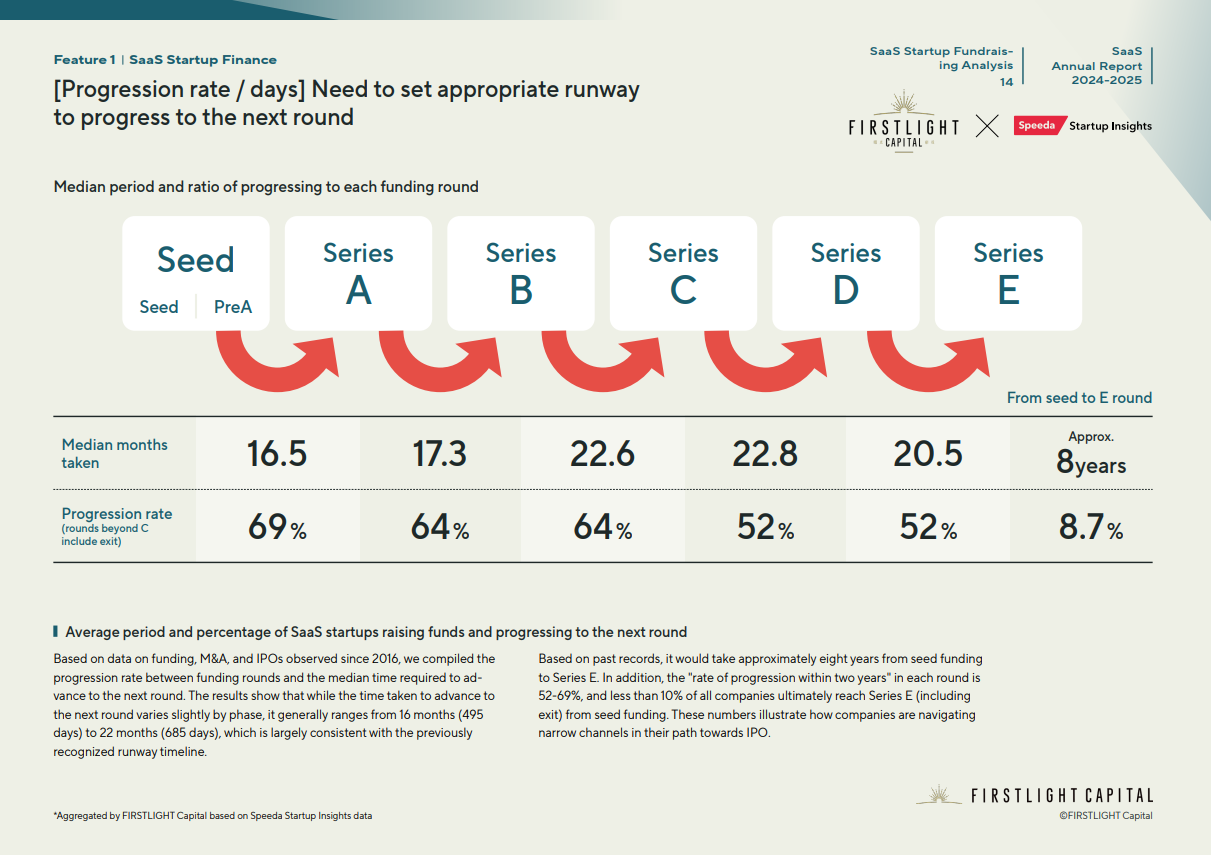

9. [Progression rate / days] Need to set appropriate runway to progress to the next round

Based on data on funding, M&A, and IPOs observed since 2016, we compiled the progression rate between funding rounds and the median time required to advance to the next round.

The results show that while the time taken to advance to the next round varies slightly by phase, it generally ranges from 16 months (495 days) to 22 months (685 days), which is largely consistent with the previously recognized runway timeline.

Based on past records, it would take approximately eight years from seed funding to Series E. In addition, the “rate of progression within two years” in each round is 52-69%, and less than 10% of all companies ultimately reach Series E (including exit) from seed funding.

These numbers illustrate how companies are navigating narrow channels in their path towards IPO.

– Feature 2 – Japan’s AI Startups: Status and Paths to Success

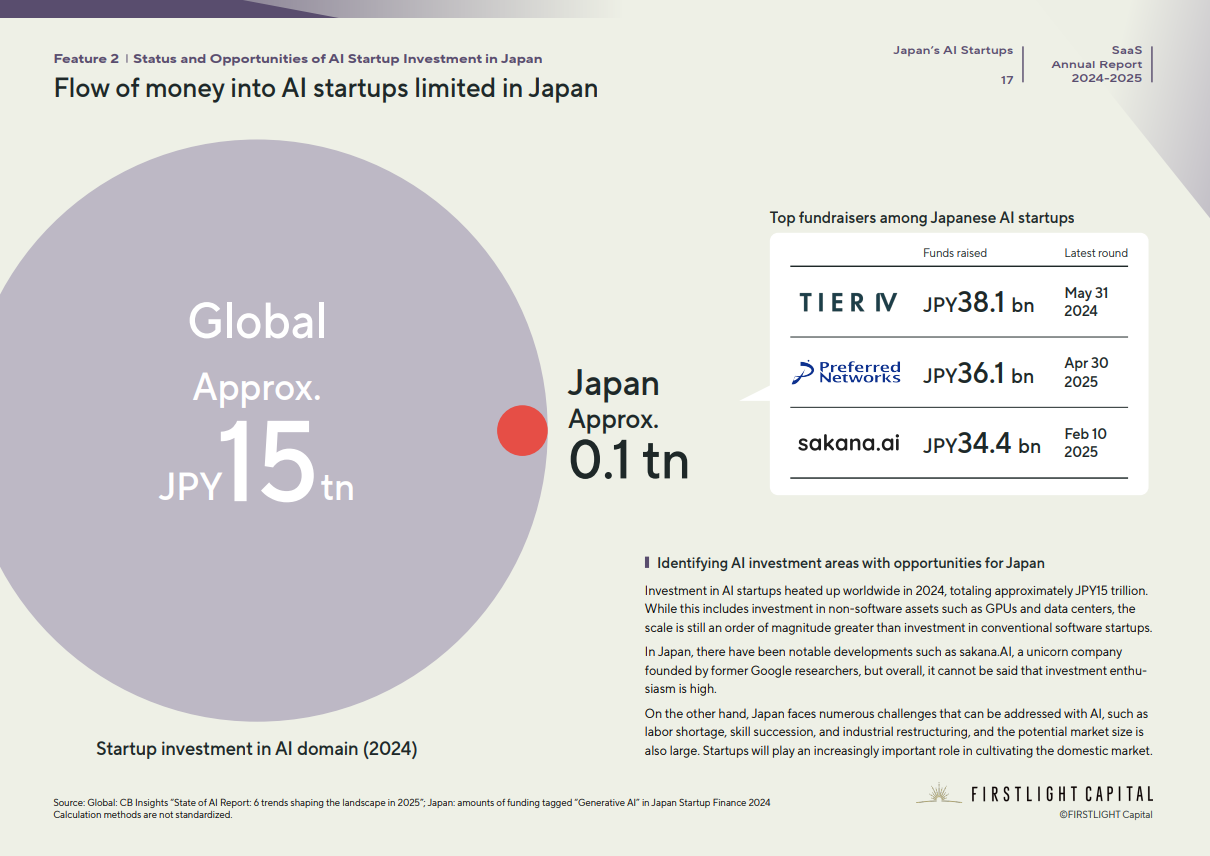

10. Flow of money into AI startups limited in Japan

Investment in AI startups heated up worldwide in 2024, totaling approximately JPY15 trillion.

While this includes investment in non-software assets such as GPUs and data centers, the scale is still an order of magnitude greater than investment in conventional software startups.

In Japan, there have been notable developments such as sakana.AI, a unicorn company founded by former Google researchers, but overall, it cannot be said that investment enthusiasm is high.

On the other hand, Japan faces numerous challenges that can be addressed with AI, such as labor shortage, skill succession, and industrial restructuring, and the potential market size is also large. Startups will play an increasingly important role in cultivating the domestic market.

Download full report (free) / Disclaimer

You can download the full report (24 pages) by submitting the form below.

We are committed to managing and protecting your personal information we receive in the manner stated below. By continuing, you agree to the following:

[Collection, Use, and Provision of Personal Information]

FIRSTLIGHT Capital, Inc. (“the Company”) may use your personal information to send you this report, to inform you of our next content release, to distribute our email newsletter, to invite you to events hosted by us, to identify and consider potential portfolio companies and LPs, and to respond to your inquiries.

[Provision of Personal Information to Third Parties]

The Company will not provide your personal information to any third party, except with your consent or in accordance with laws and regulations.

[Personal Information Protection Policy]

Please refer to the following link for details of the Company’s personal information management.

https://firstlight-cap.com/en/privacy/

Overall Direction

CEO/Managing Partner Osamu Iwasawa

Managing Partner Chiamin Lai

Chief Analyst Akio Hayafune

Entrepreneur-in-Residence Yamato Abe

Editing, Research, Production Assistance

Entrepreneur-in-Residence Takuya Maehashi

Intern Ryuho Nakano

Data provision support

Uzabase, Inc. Data Strategy Team Team Leader Takeshi Fukui

Design

Hajime Aomatsu (sukku)

Data References

INITAIL:https://initial.inc/

Next SaaS Media Primary:https://note.com/_funeo

Here at FIRSTLIGHT Capital, we regularly deliver useful content on both Japanese and global startup trends, as well as hands-on experience from our very own venture capitalists and specialists. Please feel free to contact us via the CONTACT page if you would like to be in touch. Click here to follow FIRSTLIGHT Capital’s SNS account!